Articles24 Nov 2022

Autumn Statement – Duty Tariffs

Temporarily suspension on duty tariffs on over 100 types of goods imported to UK

Articles

A summary of Brexit changes and how to report when completing VAT returns

The deadline for the first full VAT period following the Brexit post-transition period is fast approaching, 7th May. Therefore, in this article, we have summarised the effect of Brexit changes and how to report these when completing VAT returns.

We have also written many articles on Brexit. Please refer to these for more details, links provided below, and many more on our website.

Quick checklist

It is worth considering the following to get the VAT right:

VAT on Services

Except for some specific services e.g., digital services, performance, land related services, use and enjoyment override, there are no changes to VAT treatment, the place of supply rule still applies.

Please see our articles for more details

14 Jan. VAT rules for services post Brexit

16 Dec. VAT MOSS changes

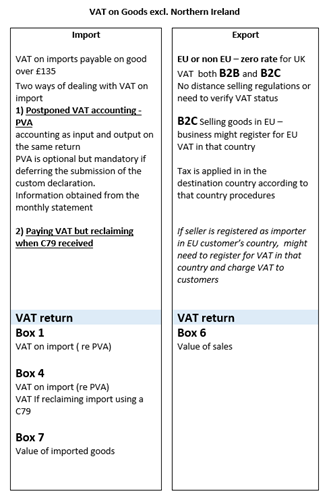

VAT on Import/Export

The most significant change from 1 January relates to the movement of goods between Great Britain (GB) and the European Union (EU).

For goods imported into GB and goods imported into NI from outside the EU, there are changes to the way a business can decide to account for and pay import VAT, as detailed in our articles listed below.

Here is the summary of changes.

For more information on postponed VAT accounting, please see our articles …

14 Jan. VAT changes for foreign mail order sellers

14 Jan. Completing your VAT return post Brexit

14 Jan. VAT rules for goods post Brexit

14 Jan. VAT rules for services post Brexit

13 Jan. Is this the death of distance selling for VAT?

14 Dec. VAT Rules for Services

11 Dec. VAT Rules for Movement of Goods

VAT return

The VAT return has also slightly changed as selling goods to EU are no longer classed as EU despatches, these goods are exports and buying goods from EU are no longer classed as EU acquisitions, these goods are imports. HMRC has renamed the VAT boxes, summary below.

Box 1 VAT due in the period on sales and other outputs

Box 2 VAT due in the period on acquisitions of goods made in Northern Ireland from EU Member States

Box 3 Total VAT due (the sum of boxes 1 and 2)

Box 4 VAT reclaimed in the period on purchases and other inputs (including acquisitions in Northern Ireland from EU member states)

Box 5 VAT to Pay HMRC

Sales and Purchases Excluding VAT

Box 6 Total value of sales and all other outputs excluding any VAT

Box 7 Total value of purchases and all other inputs excluding any VAT

EC Supplies and Purchases Excluding VAT

Box 8 Total value of supplies of goods and related costs (excluding VAT) from Northern Ireland to EU Member States

Box 9 Total value of acquisitions of goods and related costs (excluding VAT) from EU Member States to Northern Ireland

If you require more informantion, please do contact us.

More & Other Musings

View all related contentArticles24 Nov 2022

Temporarily suspension on duty tariffs on over 100 types of goods imported to UK

Articles4 Jan 2022

Full customs declarations for all goods arriving to the UK from the EU

Articles17 Dec 2021

The DIT announce a trade deal with Australia

Articles11 Dec 2021

You may be experiencing some of these common problems

Articles12 Nov 2021

An update to the £135 rule regarding VAT import post-Brexit