New Common Reporting Standard (CRS) Registration Deadline Approaching

A significant, mandatory change to the Automatic Exchange Of Information (AEOI) rules under the Common Reporting Standard (CRS) is now in effect. Affected Trustees and Directors need to register by 31 December 2025.

11 Dec 2025

An important announcement for Trustees and Directors: A significant, mandatory change to the Automatic Exchange Of Information (AEOI) rules under the Common Reporting Standard (CRS) is now in effect. You must register by 31 December 2025, or face a potential penalty of up to £1,000 for late registration.

Why the New Rules?

The UK Government is updating its regulations to strengthen the implementation of the OECD’s CRS and the US Foreign Account Tax Compliance Act (FATCA).

The core of this legislation places reporting duties on “Financial Institutions” to:

Identify specific client accounts to combat global tax evasion; and

Gather and report prescribed financial data to HM Revenue and Customs (HMRC).

The Challenge: The Broad Definition of a ‘Financial Institution’

The term “Reporting Financial Institution” is much wider than just banks and investment houses. Crucially, it now ensnares many trusts, partnerships, and investment companies that meet the “financial assets test.”

What is the Financial Assets Test?

An entity meets the test if more than 50% of its gross income is derived from activities like investing, reinvesting, or trading in financial assets.

Financial assets are widely defined, but they do not include direct interests in real property (land/buildings) or cash held for operational purposes.

The Management Trap: Managed Investment Entities

Many entities that meet the financial assets test are caught because they are considered “Managed Investment Entities.” This occurs if a Financial Institution (like an investment manager, bank, or even certain corporate trustees) has discretionary authority (directly or through another service provider) to manage, at least in part, the entity’s assets.

Real-World Examples of Entities That Must Register

These common structures are frequently overlooked but are now likely to be classed as Reporting Financial Institutions:

Structure

Why It’s Caught (The “Human” Reason)

Investment Partnerships/LLPs

If the partnership’s primary purpose is investing in stocks, bonds, or other financial assets, and a separate corporate entity (a Financial Institution) manages those investments, it must register.

Family Trust with a Corporate Trustee

Even if the corporate trustee doesn’t charge fees directly, if its related law firm or professional service provider charges fees for asset management services, the trust is considered managed by a Financial Institution and must report.

Trust with a Mixed Portfolio

A trust holding both properties and a share portfolio managed by an investment firm. If the income from the managed share portfolio is more than 50% of the trust’s total gross income, the trust is now a Reporting Financial Institution.

Family Investment Company (FIC)

If the company’s income is primarily generated from its investment portfolio, and a third-party firm handles the investment decisions on a discretionary basis, the FIC must register. (Note: If the directors make all investment decisions themselves, this specific type of discretionary management may not apply.)

Special Case: Trustee-Documented Trusts (TDTs)

A TDT is a trust where the trustee is already a Reporting Financial Institution and takes on the responsibility to report all necessary account information. While a TDT is technically a Non-Reporting Financial Institution, it is still required to complete the registration process. The registration deadline for TDTs is the later of December 31, 2025, or January 31 following the year they first qualify as a TDT.

How to Complete the Mandatory Registration

To register for AEOI under the CRS with HMRC:

Obtain a Government Gateway ID: You must have a valid Government Gateway user ID and password. You can create one easily if you don’t already have one.

Select Account Type: When registering, ensure you select ‘organisation’ as your account type.

Confirm New Registration: When prompted, you must confirm that you have ‘no’ when asked if you have registered for AEOI before.

Completing Your Registration: Required Information

To successfully register your entity with HMRC’s Automatic Exchange Of Information (AEOI) service, you will need to gather the following details:

Entity Details: The full name of the Reporting Financial Institution (e.g., the trust or investment company).

Contact Information:

First name and last name of the contact person within the financial institution.

Telephone number.

Email address.

Location: The address of the entity’s principal place of business.

Tax Identifier: The entity’s Unique Taxpayer Reference (UTR), National Insurance Number (NINO), or an indication that the Reporting Financial Institution does not have a UK tax identifier.

FATCA Identifier (if applicable):

The Global Intermediary Identification Number (GIIN) if the entity reports under the US Foreign Account Tax Compliance Act (FATCA).

If no GIIN is held, you must use the placeholder: 000000.00000.LE.000

Special Note for Trustee-Documented Trusts (TDTs)

When registering a TDT, the TDT itself must be listed as the Reporting Financial Institution, not the managing trustee. The reporting trustee should, however, be named as the primary contact person.

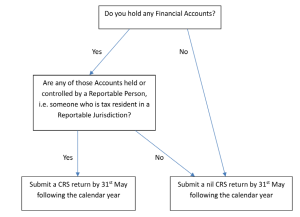

This flowchart illustrates the definition of Reporting Financial Institutions:

What Happens After Registration? The Annual Report

Once registered, the entity may face an annual reporting requirement. While the specifics of this requirement are complex, the broad principle concerning non-reporting is straightforward:

The ‘Nil Return’ Exemption

If your registered entity has no Reportable Accounts, meaning no connection to other jurisdictions (all connected persons are solely UK residents), there is currently no obligation to submit a nil return each year.

Therefore, entities that are exclusively connected to the UK do not need to submit an annual CRS return, though they remain registered Reporting Financial Institutions.

Why the gaming industry is bigger, more complex and more commercially significant than ever and why the right financial advice can help businesses stay ahead of the game.

The resignation on Monday 22 June of Sir Keir Starmer, timed for shortly before the (delayed) arrival at Euston of former mayor of Manchester, now MP for Makerfield Andy Burnham, could mark a major change in UK fiscal and economic policy.

Unless opted out, pensioners will have received the winter fuel payment for 2025/26, but it is recoverable by HMRC if income exceeds £35,000. HMRC guidance on the recovery process has recently been updated.